You Don’t Need Millions to Build Wealth in Real Estate: BRRRR Strategy Explained

When people imagine real estate investors, they tend to picture the same image: a man in a suit with a big watch, closing on his fifth apartment complex of the year, writing checks with more zeros than most of us will ever see.

It’s easy to believe real estate is a game for the already wealthy—you need hundreds of thousands in cash at all times, a perfect credit score, and deep connections to even get started.

The truth is, that image is (mostly) a myth.

In reality, the vast majority of rental properties in America aren’t owned by massive corporations or Wall Street-backed firms. They’re owned by ordinary people who started with a single property and built from there.

These small-scale landlords, often called “mom-and-pop investors,” own the majority of the single-family rental homes in the U.S. In fact, they own roughly 80% of the entire single-family rental market. That means most of the homes rented out today were purchased by people who started with far less than a million dollars — often closer to $25,000–$50,000 in initial savings.

So, how do they do it? How do everyday people quietly build portfolios that generate steady income, create wealth, and offer financial independence all without winning the lottery or inheriting a fortune?

The short answer: they use leverage, repeatable systems, and time to their advantage.

Let’s break down exactly how.

Leverage: The Great Equalizer

How a small down payment lets everyday investors build wealth faster.

In most investments, your money controls exactly what it’s worth. If you have $10,000 and you buy stocks, you control $10,000 worth of assets.

But real estate plays by a different set of rules.

Through financing, typically a mortgage, you can use your $10,000 or $20,000 down payment to control an asset worth five times as much. That’s called leverage, and it’s one of the most powerful wealth-building tools available to small investors.

Let’s look at a simple example:

You buy a $200,000 rental property with a 20% down payment ($40,000). The bank lends you the remaining $160,000.

Now, if the property appreciates just 3% per year, it increases in value by $6,000 annually. That’s not much, until you realize your $6,000 gain came from an initial investment of only $40,000.

That’s a 15% return on your equity, before accounting for any rental income.

No stock, bond, or index fund can safely replicate that kind of leveraged compounding for the average person.

And here’s the kicker: the tenant’s rent pays down your loan. So while your property appreciates in value, someone else is helping you pay it off.

You’re effectively using other people’s money (the bank’s) and other people’s income (the tenant’s) to grow your wealth while maintaining ownership of the appreciating asset.

That’s the power of leverage. It turns a modest starting capital into a snowball that grows faster every year.

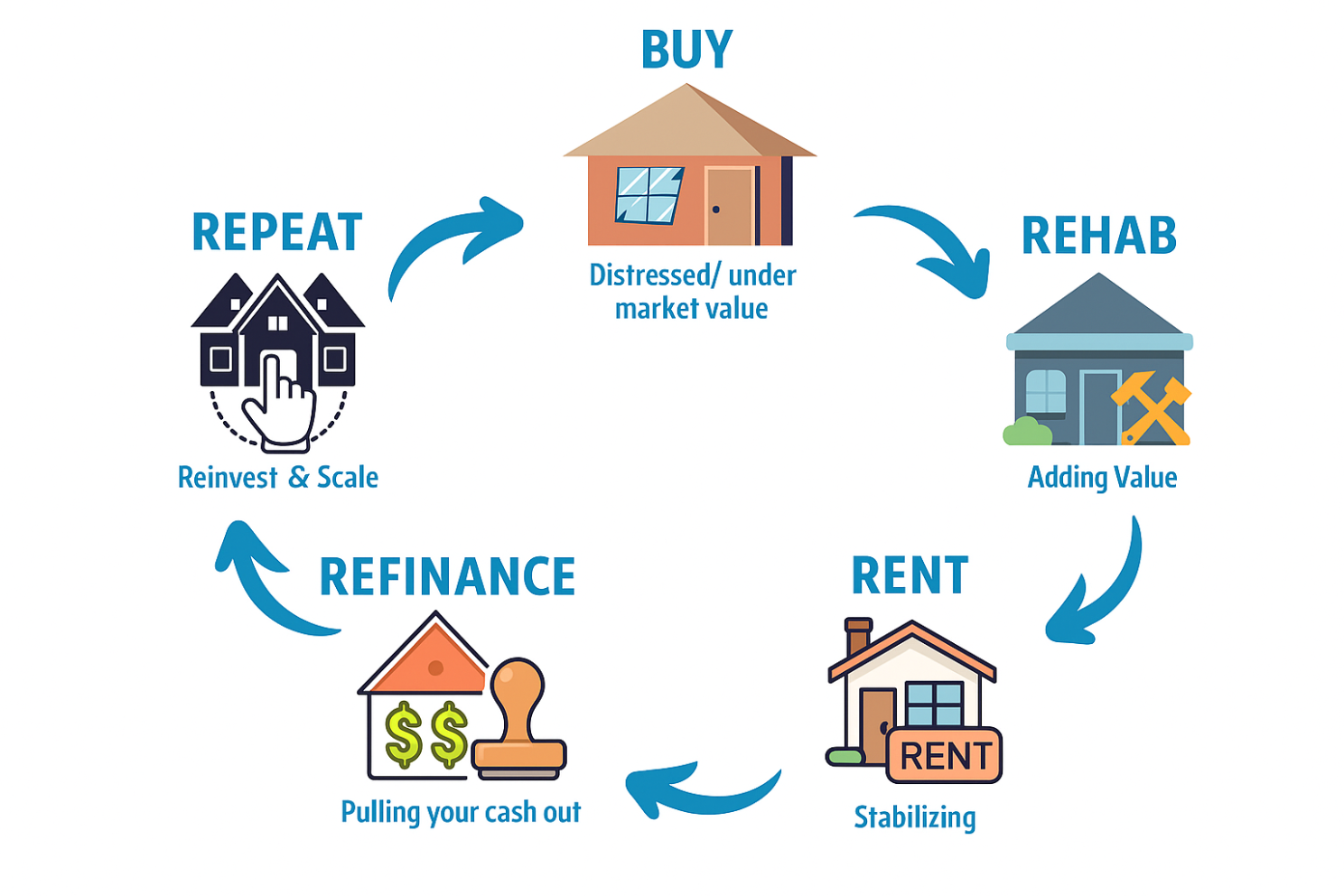

The BRRRR Strategy: How Small Investors Unlock Big Gains

This strategy lets small investors reuse the same funds to build bigger portfolios and accelerate long-term wealth.

BRRRR stands for: Buy → Rehab → Rent → Refinance → Repeat

This strategy isn’t a gimmick; it's how successful players recycle the same capital across multiple deals.

Here’s how it works in real numbers:

- You buy a distressed property for $120,000. (With financing through a hard money lender [HML])

- You spend $30,000 rehabbing it. (Again, the HML loan should include renovation costs; you dont need to spend your own capital if you don’t have it.)

- All in, you’ve invested the initial 20% of the HML (30,000), plus whatever interest needs to be paid off, so say another 15,000. You’re sitting at 45,000 invested.

- Once it’s rented and stabilized, it appraises at $200,000. Now you can refinance with a traditional mortgage on the property.

The bank may lend you 75% of that new value ($150,000). You pull out most or all of your initial investment while still owning the property.

You then take that same $30,000–$40,000 and go do it again.

Each time you recycle your money, your portfolio grows exponentially.

The BRRRR is the reason many ordinary people can build multi-property portfolios using the same initial pile of cash over and over again.

Of course, the strategy requires discipline. Proper appraisals, conservative numbers, patience, and strong relationships with all parties involved.

Never force a deal. Always be able to walk away; investors get burned when they are desperate and overlook the math.

When done right, it creates a flywheel effect: each deal funds the next, compounding your returns and expanding your cash flow base.

Compound Equity Growth: The Silent Wealth Builder

How steady appreciation and loan paydown build momentum and equity snowballs into lasting wealth.

The third piece of the puzzle is something few investors truly appreciate until years later: equity compounding.

Let’s take the same $200,000 property example.

You put down $40,000 and finance the rest. If your tenant’s rent covers your mortgage, insurance, taxes, and maintenance, you’re essentially holding the property at break-even or slight positive cash flow.

Now, what happens over five years?

- The mortgage principal goes down by roughly $10,000–$12,000.

- The property appreciates modestly at 3% annually, reaching around $232,000. Note: appreciation is closer to 4-5% nationally, but being conservative when it comes to investment is always best.

- That’s $32,000 in appreciation plus the loan paydown.

Total equity gained: around $42,000. Nearly your entire original investment, doubled through a short period of time.

This is where real wealth begins to snowball.

Even modest investors who repeat this process every few years can end up with seven figures of equity within a couple of decades by understanding how time and leverage are amplifiers for wealth.

Risk, Discipline, and the Long Game

Why winning investors prioritize math and patience, protect their cash flow, and treat investments like a business, not a gamble.

Of course, leverage cuts both ways. If property values drop or you overpay, you can find yourself overextended.

That’s why small investors who win long-term focus on cash flow and fundamentals.

The math always comes first.

Before buying, they ask:

- Will this property rent for at least 1% of its purchase price per month?

- After all costs, am I still cash-flow positive?

- Do I have reserves for maintenance and vacancy? This is big for first time investors. If you spend every last penny on a property, you wont be in good shape for emergencies. Always make responsible financial decisions, just like you would with personal purchases.

You might not see 10x returns overnight. But you’ll own assets that appreciate, generate income, and protect you from inflation—something cash in a savings account will never do.

Start Small, Learn Fast, Scale Smart.

Why starting slow gives you the flexibility to make mistakes, build relationships, and create the systems needed for long-term growth.

Here’s the thing most people don’t realize: starting small is actually an advantage.

When you only own one or two properties, you can be nimble. You can self-manage, make personal improvements, and learn the ropes without risking a fortune.

You’ll inevitably make mistakes; every investor does, but the goal is for them to be small, recoverable ones.

You’ll learn how to screen tenants, vet contractors, read inspection reports, and handle unexpected costs.

You’ll also begin building relationships that compound over time, including networks of wholesalers, contractors, lenders, and agents.

Real estate rewards reputation. The earlier you start, the more years you have for those connections to mature.

And once you’ve survived your first few deals, you’ll realize something: It’s not about the dollar amount. It’s about the systems, habits, and people you’ve built around the process.

That’s what makes you scalable.

Why This Matters

In today’s market, institutional investors are making headlines—but local investors still drive the majority of residential investment transactions, around 75-80%.

And they’re needed.

When individuals buy and improve older homes, they stabilize neighborhoods. They create affordable housing. They keep ownership local, rather than consolidating it under national funds.

Every time a mom-and-pop investor renovates a duplex or saves a foreclosure, they’re

building wealth and contributing to the health of the community.

That’s something no spreadsheet in a hedge fund office can replicate.

Final Thoughts

You don’t need to be rich to start. You need to start smart.

Understand leverage. Master the math.

Think long-term.

Every million-dollar portfolio starts with one small deal and one person willing to take the first step.

Start where you are, with what you have, and focus on momentum over magnitude.

In real estate, wealth isn’t built by who starts with the most money, it’s built by those who stay in the game the longest.