The Must-Have Skill For Every Real Estate Investor

Investing in residential properties can be a fantastic way to build long-term wealth—if you understand the numbers behind the deal. Underwriting (analyzing the deal’s financials) is critical, especially in a local-heavy investor market like Southeastern Wisconsin. To capitalize when opportunities are present, investors must follow a disciplined approach.

In this short article, we outline tangible, easy-to-follow best practices for underwriting standard residential real estate investments, with a focus on the Milwaukee area market.

Knowing the Market

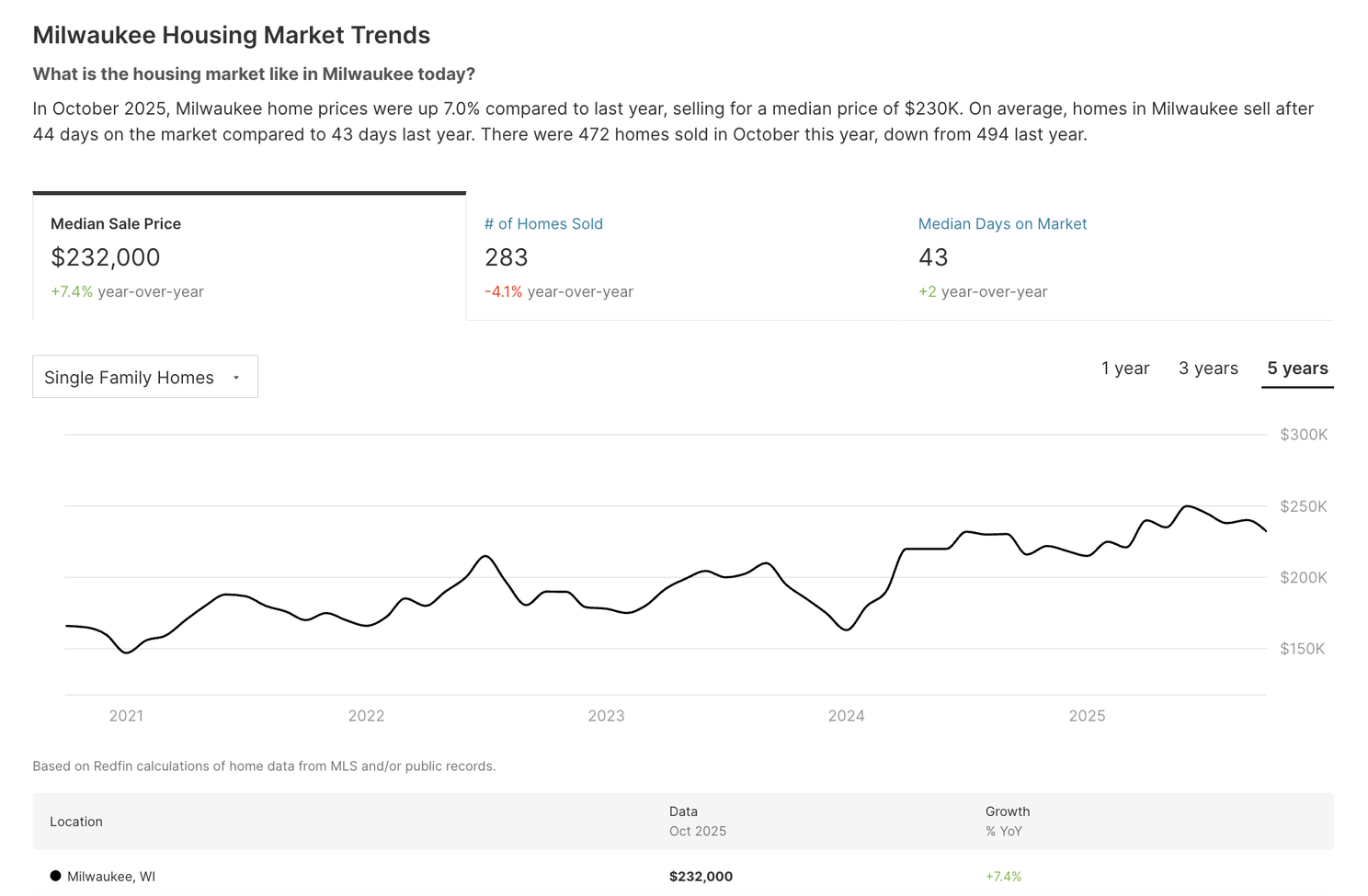

Before diving into numbers, get acquainted with market trends and neighborhoods. Real estate follows general patterns, but the nuance is hyper-local, and Milwaukee’s market has its own quirks and dynamics.

Below is a quick list of items to stay up-to-date with in your investment market:

- Home values & appreciation trends

- Rental demand trends

- Typical rents

- Property taxes

- Tax legislation

- Demographic trends

By grounding yourself in these items, you’ll avoid basing your deal on unrealistic or outdated assumptions. Next, let’s get into the 5-step analysis process.

1 | Determining the Current Market Value

Mastering Comps: The foundation of every good deal

The first step in underwriting is figuring out what a property is truly worth today. Don’t take the seller’s word for it; find the comps (comparable sales).

To do this, use these methods:

- Use the MLS or Online Sales Data: The Multiple Listing Service (MLS) is the most comprehensive source for accurate comps in Wisconsin. If you’re working with a realtor or broker, have them pull a Comparative Market Analysis (CMA) with recent sales. If you’re on your own, websites like Redfin or Zillow can show recent sold prices; these aren’t as complete as the MLS, but a starting point. If you’re looking for an investor-focused tool with more complete info than Zillow, we have used and recommend PropStream.

- Match Like with Like: Identify properties similar in key features: same property type (e.g. SFH vs. duplex), similar age and style, comparable square footage (within ~10–15% ), and similar condition. Pay close attention to the condition, especially key areas such as the kitchen and bathroom. Adjust your estimates based on whether the property is distressed, average, or updated.

- Stay Local and Recent: The first two points are pretty straightforward and commonsensical for those with even minimal experience with real estate, but this next point is where more people get lost.

Real estate values can vary street by street. Make sure to use comps in the same subdivision or neighborhood, ideally within a quarter to half mile. A good rule of thumb here is to try to never cross major roads when finding comps. This isn’t just about highways; focus on staying on the same side of high-traffic roads and even the Milwaukee River.

Also, stick to the last few months of data; Milwaukee’s market has strong seasonality (spring/summer are more active) and an upward trend, so values from a year ago may be inaccurate.

Doing your homework on market value protects you from overpaying, and doing so keeps you on track for long-term success.

2 | Estimating Rental Income

Establish rents on comparable units and always budget for tenant turnover

Rental properties live or die by their rent rolls, so take a realistic look at what you can earn and how consistently you can earn it.

- Survey the Rent Comps: Just as with home values, look for rental comparables. Check what similar units are renting for in that area right now. You can use tools like Rentometer to get quick rent estimates by bedroom count and ZIP code. Also consider checking current listings on Zillow, Craigslist, or even Facebook Groups to see asking rents for comparable properties.

- Consider the Neighborhood and Property Class: Neighborhoods vary. A duplex in a high-demand area like Bay View or the East Side will likely command top-dollar rent, whereas a similar duplex in a less trendy area might need to be priced more moderately. Also, property condition matters: newly renovated units with modern amenities get higher rents; dated or lower-grade units may need a discount to fill. Align your rent projections with the property’s class (A, B, or C) and local median incomes.

- Account for Vacancy: Even in a strong Milwaukee market with 94% occupancy, no property is rented 100% of the time. Tenants move out, repairs happen, and you might need a month or two to find a new tenant. A common practice is to assume a vacancy rate of about 5% (which equals roughly half a month per year vacant). In Milwaukee’s tight market, you might experience less vacancy, but it’s prudent to budget for some downtime. If you never need it, great; there's extra cash. But if you do, you’ll be glad you planned for it.

- Miscellaneous fees: When evaluating a property, keep in mind alternative income sources. If there is a garage or parking slab for a multi-unit property, parking is a source of income. Other fees, such as pet fees or laundry, can boost your monthly income as well. As with the rent, make sure to estimate conservatively.

By using realistic rent figures and stress-testing with a vacancy allowance, you ensure your deal has a cushion. Overestimating rent or assuming zero vacancy is a recipe for trouble, so stay conservative on this front.

3 | Calculating the After-Repair Value

Separate “as-is” and “as-improved” values in your analysis.

Many of the best deals for new investors are value-add opportunities; these are ways to build significant equity in months. In these cases, you shouldn’t just look at the current value but also, and more importantly, the after-repair value (ARV).

Note: this section doesn’t apply to all properties; if you strictly invest in turnkey, skip to step 4.

Here’s how to approach ARV analysis:

- Envision the End State: Determine what level of rehab or upgrades you plan to do. Is this a light cosmetic update (paint, etc), or a major renovation (new roof, kitchen/bath gut)? The ARV should be based on comps in close proximity and improved condition.

- Get Repair Estimates: Your ARV is only as good as your understanding of what it takes to get there. The best investors have an acute understanding of the rehab costs. Obtain contractor bids for your first several properties, and eventually, you'll be able to ballpark like a vet. Be thorough: include all expected repairs/upgrades (plus a “wiggle room” budget; most investors we know add an extra 10k or 10%, whichever is greater). Ensure your rehab strategy aligns with the neighborhood. Bay View-like areas will require nicer finishes, but less desirable areas won’t require such nice finishes.

Determining ARV is crucial for any strategy, flips, BRRRR, and even buy-and-holds.

4. Finding the Right Financing Strategy

Your loan strategy shapes the deal from day one; choose carefully.

Underwriting isn’t complete until you incorporate how you’ll finance both the purchase and the rehab.

Choose financing that fits the project. The type of loan or financing you use significantly affects your underwriting cash flow and costs. Two of the most common routes for small investors are:

- Conventional Mortgage: Once the property is in good shape or if it's turnkey at purchase, a 30-year fixed mortgage might be the go-to. Rates in 2024–2025 have been around 6-7% for investment loans, which is higher than a few years ago but still reasonable. Your analysis should include the payment, taxes, and insurance as monthly costs.

- Hard Money Loan: If the property needs work beyond minor cosmetics for a couple grand, a Hard Money Loan (HML) can finance the purchase and repairs, typically around 70-80% of the total cost. Because HMLs typically have higher rates around 10-12%, you should use HML to acquire and fix the property quickly, then once it’s rented and stabilized, refinance into a traditional mortgage. This strategy is common for BRRRR deals. When underwriting, you must account for the carrying costs of that expensive short-term loan (interest, points, and loan fees) in your total investment.

- DSCR Loan: For rental properties that are already generating income or expected to do so quickly, a DSCR (Debt Service Coverage Ratio) loan can be a strong option. Instead of relying on your personal income, lenders evaluate the property's ability to cover its own debt by comparing the rental income to the mortgage payment. Most lenders look for a DSCR of at least 1.0–1.2, meaning the property produces enough income to cover its monthly debt obligations with a small cushion. Rates are typically higher than conventional loans but lower than hard money, and DSCR loans offer flexible underwriting and faster closings, making them a viable middle ground.

- Consider Other Costs and Holding Expenses: During a rehab, the property won’t be generating rent, so budget for those holding costs of loan interest, utilities, insurance, property taxes, etc. Include costs for both purchase and refinance (title fees, lender fees, transfer taxes, etc.) in your overall cost stack in the underwriting.

5. Leveraging Tools and REPs (Real Estate Professionals)

Combine digital tools with realtor and lender insight for stronger analysis.

It may seem like we covered a lot, and this was just an overview. Underwriting can feel overwhelming to new investors, but fear not, you don’t have to do it all manually. There are plenty of tools and resources to make the process easier and more accurate.

Some good starters are listed below.

- Deal Analysis Spreadsheets: Use a rental property analysis spreadsheet or calculator to input all your numbers. These spreadsheets (many are free online) will automatically compute your cash flow, ROI, cap rate, etc., and often include line items you might forget. For example, Innago (a property management software) offers a free rental property analysis spreadsheet template that helps you plug in purchase price, rehab costs, rents, and expenses to evaluate a deal’s cash flow.

- Online Calculators: Websites like BiggerPockets have deal analyzers that provide metrics like cash-on-cash return, monthly cash flow, and even long-term projections. Some of these require a membership, but even a trial could be used for a few deals as you learn.

- Rent Comp Services: We mentioned Rentometer for rents; it’s great for quick rent checks. Also consider talking to local property managers and checking Zillow “for rents.” Don’t hesitate to reach out to these people; their input is valuable for underwriting purposes, and many will be happy to share their two cents.

Tools like these ensure you follow a systematic approach every time.

Lastly, consider building relationships with real estate agents and lenders who understand investment properties. An investor-friendly agent can feed you comps and insight for underwriting, and an investor-friendly lender can pre-approve you with a certain loan structure in mind.

Treat underwriting as an ongoing learning process that you will get better at over time.

The more tools you use and people you have on your team, the more refined your analyses will become.

Conclusion: Underwrite Like a Pro, Invest with Confidence

Underwriting may not be the most glamorous part of real estate investing, but it is absolutely paramount for success. By diligently analyzing the pieces of the puzzle, you take the emotion and guesswork out of the equation, increasing your odds for long-term success.

For a new investor in Milwaukee or anywhere in Wisconsin, sticking to these best practices will help ensure you’re buying properties that make sense on paper and in practice.

If a deal doesn’t meet your numbers, be willing to walk away. Always set a firm max dollar amount; don’t let ego get involved in a bidding war. It’s far better to pass on a deal than be impatient and regret it later.

Underwriting is a skill that gets easier with practice. Be objective, use data, and don’t stray from your core metrics to justify a deal.

Even if it's not as entertaining as a walkthrough or deal search, sit down with the numbers and work through the analysis carefully. If you follow the steps outlined, you’ll be well on your way to building a profitable rental portfolio.

Consistent, disciplined underwriting today sets you up for stronger results down the road.

Happy investing!