FinCEN’s Big Scary New Rule: What Investors Need to Know

A Major Change Coming in 2026

Starting March 1, 2026, the U.S. Treasury’s Financial Crimes Enforcement Network (FinCEN) will enforce a nationwide rule requiring title companies to report all cash or non-bank-financed residential real estate deals involving LLCs, trusts, or other entities.

The goal: stop money laundering through anonymous property purchases. The effect: longer closings, more headaches, and more deals falling through if you don't know what you're doing.

If you’re a real estate investor or wholesaler, this rule will change how your transactions are handled.

What the Rule Covers

A brief overview

Formally called “Anti-Money Laundering Regulations for Residential Real Estate Transfers,” it applies to:

- Residential property (1–4 units, condos, townhomes, vacant land)

- Non-financed deals (cash, seller financing, hard/private money loans)

- Purchases by entities like LLCs or trusts

There’s no minimum purchase price; a $50K lot and a $5M mansion are treated the same.

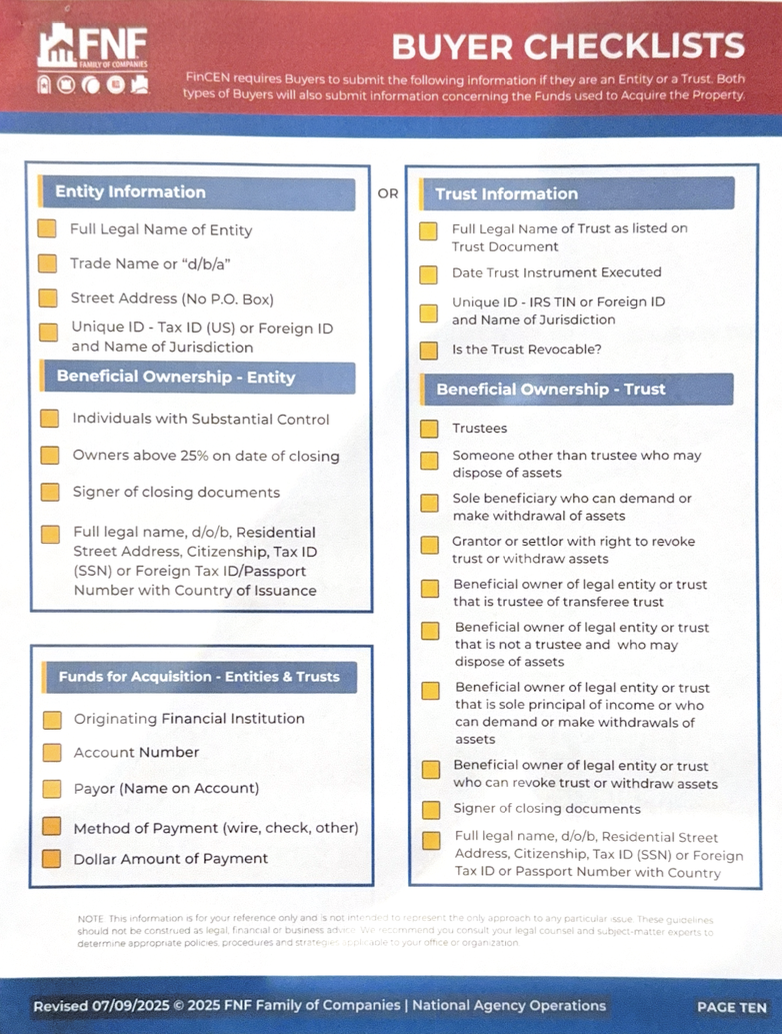

Title companies must now report:

- Buyer & seller identities: personal info of anyone who holds a 25% or greater stake in the entity. This includes SSN/driver's license, full legal name, and address.

- Funding sources: all wires, checks, and bank accounts involved.

Reports are due to FinCEN within 30 days of closing and filed by the title or settlement agent, but you will have to fill out the information on an online portal; no paper allowed.

Impact on Investors

Investors' workflows will change, but it shouldn’t break your business.

The concern for investors is plentiful. Here are the most significant items to note:

- Less anonymity: LLCs and trusts will have to disclose owners’ names, addresses, SSNs, and IDs.

- More paperwork: Expect to verify identities, funding sources, and provide supporting documents before closing.

- Slower closings: Title agents will need time to collect and verify data.

- Wholesalers: Assignment buyers using LLCs or cash must now provide full disclosure. Set expectations early to avoid delays and prevent deals from falling through.

- Private & hard money loans: Still count as “cash” under the rule, meaning they’re reportable.

In short, investors will face more compliance steps. However, legitimate operators should adapt easily; this isn’t going to break your business. The aim is to clean up the market and prevent money laundering from foreign and domestic parties. In fact, in some areas, this may improve affordability, as these illegal actors tend to overbid on listed properties.

Big New Risk: Title Companies

Why Choosing the Right Title Company Matters More Than Ever

With all this new data being collected, your title company becomes a gatekeeper of sensitive personal and financial information. Choose one that:

- Uses encrypted portals (not email) for ID and bank data

- Has strong cybersecurity and fraud prevention systems

- Is trained in FinCEN compliance to avoid mistakes or delays

Low-cost or inexperienced firms may not be prepared for these new demands, which puts you at risk for delays, reporting errors, or even data leaks. The best title companies are already adapting, training staff, and updating systems to protect clients.

Preparing for the Changes

March 2026 might feel far off, but smart investors and real estate professionals are preparing now. Here are a few steps to make sure you’re ready when the new rules kick in:

- Stay Informed: Keep up with updates from FinCEN and industry news. FinCEN is rolling out educational resources like FAQs, webinars, and even brochures to help everyone understand the new requirements. Consider subscribing to FinCEN’s update alerts.

- Organize Your Entities: If you buy properties through LLCs or trusts, use the lead-up time to get your beneficial owner information organized. Have updated addresses, Social Security or EIN numbers, and ID copies for the beneficial owners ready to go. This way, when it’s time to close a deal, you can promptly provide the necessary details. No one wants a scramble on closing day to track down a co-owner’s birthdate or ID.

- Talk to Your Title/Escrow Agent Early: The moment you start working on a deal that you suspect will trigger FinCEN reporting, loop in your title company and ask about their process. A good title agent might send you a checklist of what they’ll need. By opening this dialogue early, you show that you’re a cooperative client, and you can also gauge how prepared the title company is. Being proactive can save you from closing delays or compliance hiccups.

- Educate Your Team and Partners: If you’re a wholesaler, agent, or investor who works with others, spend some time informing your network about these changes. For instance, if you’re an agent representing an investor or a cash buyer LLC, you should brief them. Wholesalers should ensure their buyers and sellers are aware that providing personal information will be a standard part of closing. Having these conversations in advance can build trust and avoid anyone getting cold feet when confronted with a form asking for their SSN right before closing.

Conclusion

The new FinCEN legislation is poised to bring greater transparency to real estate investing. While it means more disclosure and diligence for most parties, it’s also ushering in a safer, more regulated environment where dirty money will have a harder time hiding in real property.

By understanding the rules, preparing early, and working with the right title company, you can continue investing with confidence.

Stay informed, stay compliant, and don’t let a bit of extra paperwork scare you off from the opportunities that real estate investing still offers.